Transactional Net Margin Method (TNMM)

What you will find on this page:

-

Quick Links will be displayed here

Want to know more about the Transactional Net Margin Method (TNMM)?

Maikel Verhoeven

Managing Director

Transactional Net Margin Method (TNMM)

The Transactional Net Margin Method (TNMM) is the most popular Transfer Pricing Method. It’s widely applied across industries due to its ease of application, effectiveness, and typically reduced chance of scrutiny.

TNMM examines the net profit margin relative to a base such as costs, sales, or assets that a taxpayer realizes from a controlled transaction. It ensures that the profitability of related-party transactions aligns with the arm’s length principle—treating related parties as if they were unrelated.

TNMM is generally applied when:

- No Comparable Uncontrolled Price (CUP) exists due to unique transactions or a lack of reliable data.

- One party performs routine, low-risk functions that are easy to benchmark.

- Other methods (like Resale Minus or Cost Plus) are difficult to apply or defend.

This method is especially useful when one of the entities performs routine functions (e.g. contract manufacturing, limited-risk distribution, or shared services). with the distributor. If a distributor increases their OPEX without increasing sales, they become loss-making—keeping pressure on operational efficiency and margin discipline.

How the Transactional Net Margin Method (TNMM works

TNMM compares the operating profit (EBIT) of the tested party with the EBIT margins of comparable independent companies.

A Profit Level Indicator (PLI)—often cost-based or turnover-based—is selected depending on the function performed.

A benchmark study is conducted using financial databases to find suitable comparables.

The resulting benchmark range (e.g. median EBIT/cost margin) is used to determine if the tested party’s results are at arm’s length.

If the tested entity performs multiple routine services, a segmented P&L is prepared to evaluate each function separately.

Comparison: TNMM vs. Cost Plus

The Cost Plus Method applies a gross mark-up to, for example, costs of goods procured, while TNMM with the Net Cost Plus Margin evaluates profitability at the EBIT level on a net margin. The Operational Expenses are as such also considered for the TNMM and not for the Cost Plus Method.

| TNMM | Cost Plus |

|---|---|

| Net margin based (EBIT) | Gross margin based (before OPEX) |

| Operational expenses included | Operational expenses excluded |

| Benchmarked on EBIT/Costs or EBIT/Sales | Based on markup on direct costs |

| Used for routine functions, tested on a net basis | Used for price setting or internal cost markup |

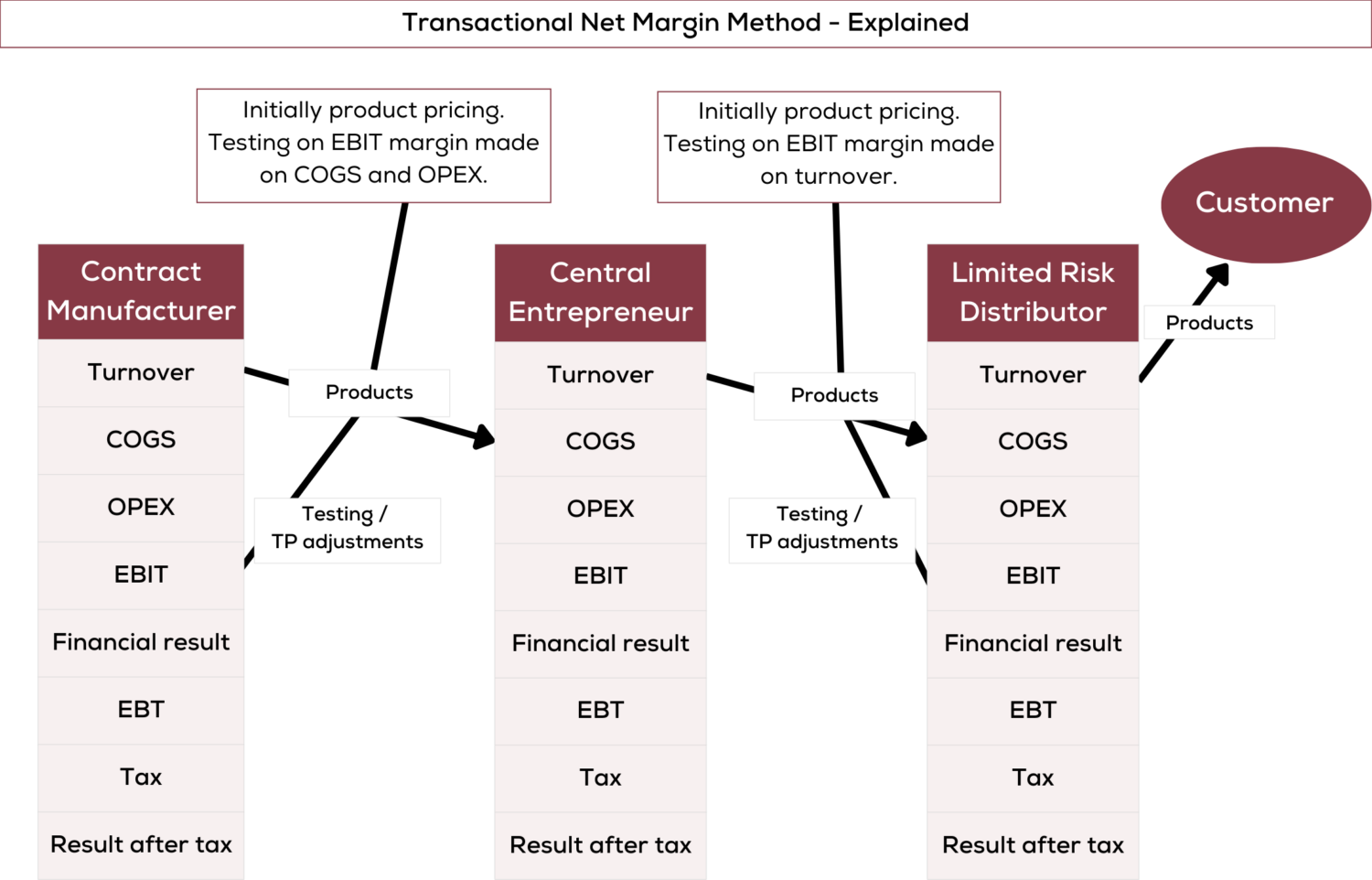

TNMM – P&L placement

TNMM testing takes place at the EBIT level. It often uses cost or turnover as the base, depending on whether the tested party is a cost center (e.g. service provider) or revenue generator (e.g. distributor).

What our clients say about us

To-the-point and tailormade support with concise reports

QG knows the ins and outs of transfer pricing and they listen well to understand our situation and provide to-the-point and tailormade support with concise reports. In addition, they have a strong local and international network of specialists that can support our OpCo’s.

Martijn van Eenennaam

Director Risk & Compliance at Vebego

Proactive and practical solutions

Quantera Global has a professional, proactive and enthusiastic transfer pricing team. I believe Quantera Global can provide many MNEs like MSI with reasonable and practical solutions in the transfer pricing field.

Kevin Wang

Managing Director at MSI

Strategic and trustworthy partner

Quantera Global is great to collaborate with, a trustworthy partner from strategy up to defense, that fully understands the complex nature of Transfer Pricing while strategically reducing risk.

Hicham Maatoug

Director Tax Emea at Celanese

Strong analysis and rationale

The analysis was thorough, easy to understand and Quantera provided strong rationale and support to modify our transfer price policy to better reflect our changing business models.

Carolyn Hauger

CFO / Senior VP at LION

Professional and timely delivery

We appreciate to work with Quantera Global. They understand what we need and deliver in time. We consider Quantera Global as a professional partner providing unique knowledge and experience.

Thom Coenen

International Tax Manager at Nutreco

Big 4-level service

Quantera Global provide a level of service and insight usually found just in the Big 4. They are responsive and knowledgeable. In a world where transfer pricing is ever more important, you need Quantera on your side.

Jason Collins

Head of Litigation, Regulatory and Tax at Pinsent Masons

Global perspective with detail

Quantera Global applies a helicopter view with an eye for detail when required, is a pleasure to work with and has a solid global network. Quantera Global is a specialized Transfer Pricing firm with a global network which I can highly recommend.

Willem Zwitserloot

CFO at Cordstrap

Expert and personable team

Quantera Global has assisted me on a complex transfer pricing topic. It was a real pleasure to work with the Quantera Team. They have the ability to combine high level senior expertise with the kind of personal touch that makes you feel at home.

Maurice Schemkes

Group Tax Manager at NS

Creative TP design

Quantera Global has been instrumental in designing and defending our transfer pricing model. They are really creative, they offer what you really need and all this comes with a human perspective.

Marie-Thérèse Josten-de Dobbelaere

Business Controller, Mayordomo Holding B.V

Trustworthy TP strategy

Quantera Global has proven to build up a trustworthy partnership with our own team. They were able to translate the sometimes complex supply chain in our Group to a logical Transfer Pricing Strategy supported by readable TP documentation.

Pim Peters

Corporate Director Tax at Marel

Skilled and empathetic execution

Quantera Global has assisted us in a specific transfer pricing project. Their way of working can be described as skilled, empathetic and fast while using proper communication skills.

Michel Schilt

CFO at TimeSeries

Professional international collaboration

Quantera Global is highly professional, motivated and communicative. They established an outstanding partnership with our international tax team to achieve the right outcome for our clients. The close collaboration helped us to grow our international tax practice substantially over the past three years.

Jasper Rijnsburger

International Tax Partner at WVDB

Practical intercompany solutions

It is a pleasure to have Quantera Global assist us in designing and setting-up our intercompany charges for our growing international activities. Meeting our needs for a practical and straightforward solution to start with, while preparing us for a future-proof approach as well.

Ramon Caanen

Partner at Gordian

Valuable first project results

I really appreciate the valuable results of our first Transfer Pricing project with Quantera Global.

Georg Proksch

Tax Manager TP Red Bull

Swift and outstanding service

Quantera Global has assisted me on various transfer pricing projects, always responding swiftly and with outstanding client service.

Eduardo Goldszal

Finance Senior Director at NCR

Concise TP advice

Quantera Global excels in transfer pricing knowledge and provides to-the-point advice.

Lars Holweg

Concern Controller at Nedap

Favorite TP team

Quantera Global is my favorite team to work with; they excel in their knowledge of transfer pricing.

Akshay Kenkre

Founder and CEO at TransPrice

Pragmatic last-minute solution

Quantera Global was able to help us last minute by suggesting a very pragmatic approach for a very complicated matter thus enabling our client to meet all their filing deadlines.

Joost van den Berg

Partner at HVK Stevens

Expert transfer pricing support

Quantera Global knows the ins and outs of transfer pricing and they listen well to understand your situation and provide to-the-point support with concise reports. In addition, they have a strong local and international network of specialists which they match well.

Jan Verhoeven

CFO at Axell Group

Reliable long-term transfer pricing partner

Quantera Global is an excellent partner in the Transfer Pricing universe. We have been working with Quantera Global The Netherlands for many years. During these engagements, the consultants had demonstrated deep knowledge at all times, to perform their work at the highest quality. They are also a group of exceptional professionals with an outstanding practical approach.

Diego Cesar Jalon

President of Losur Overseas SL

Hands-on global transfer pricing solutions

Quantera Global has assisted us with several transfer pricing projects around the globe. Their hands-on approach, and their offer which included their transfer pricing software Coperitas, has made us choose them.

Scott Muecke

Chief Accounting Officer and Controller at Tricon

Efficient compliance management

Quantera Global has lightened our compliance burden in an efficient way. We are now fully prepared in these post-BEPS times.

Stephan Gaemers

Tax Director at TIP

Specialist in reporting and guidance

Quantera Global is the specialist in transfer pricing reporting. They provide us with the extra knowledge to produce the master and local files. Communication is clear and direct.

Piet van Eekelen

Group controller at B.A. Geurts-Janssen B.V

Guided TP model improvement

Quantera has been with us since the start of the overhaul of our TP model. With the help of Quantera we were able to ask the right questions and also got the business thinking about where their value really sits. This journey has left us being much better in control. They maintain a good overview of outstanding issues and pro-actively contribute to resolve issues.

Jord Ruijgh

Head of Tax & Treasury at Meltwater

Clear and practical advice

Quantera Global has excellent knowledge of transfer pricing and understands the customer’s situation. Questions are carefully considered, so that a response is given as concretely as possible and in understandable language for the client.

Ton Rouwette

Controller Fischer Benelux B.V

Flexible TP model design

Quantera Global has invested time in understanding our business and to design and implement our transfer pricing model in a way that also our business people understand, being flexible in their solutions.

Rob van Kalkeren

Global Tax & Transfer Pricing Manager at Hendrix Genetics

Strong international network

Quantera Global knows the ins and outs of transfer pricing and they listen well to understand your situation and provide to-the-point support with concise reports. In addition, they have a strong local and international network of specialists which they match well.

Stijn Kalkers

Manager Finance & Accounting at Apex International

Trusted sparring partners

They dare to make firm statements and they keep to what they say. They are really high-level sparring partners.

Marie-Jose van Dalen

Tax Manager at Vion Food Group

Skilled and updated professionals

Quantera Global has skilled professionals with updated know how and expertise to assist international corporations to fit and comply with transfer pricing regulations.

Diego Jalon

President of Losur Overseas SL

Enabled major TP progress

Quantera Global helped us to make a major step forward in analyzing our business and intra-group transactions and made it possible to fulfill all the needs in documenting and implementing our transfer pricing policies. Without their support, it would have been impossible to meet the needs of all stakeholders (internal and external) in time!!

Ton Mens

CFO at Agio

Augmented tax advisory expertise

Quantera Global’s transfer pricing specialists have been instrumental in augmenting our tax advisory firm’s expertise in their and support in various transfer pricing cases and benchmark studies for our clients. Characteristic is their deep knowledge, clear communication, and proactive approach. We would recommend Quantera Global to anyone seeking a reliable partner to enhance their capabilities in the specialized field of transfer pricing.

Christiaan Cornet & Edgar van Hassel

Van Oers

High-quality master/local file support

Quantera helped us on preparing master file and NL local files for Anadolu Efes. We observed good technical quality, diverse experience, a team composed of both senior and young people and they’ve elaborated details more than one would expect. Thanks a lot.

Mustafa Susam

Group Tax Director at Anadolu Efes

Timely project delivery

Quantera Global has assisted us in a transfer pricing documentation project that needed to be dealt with at a short notice. We appreciate their delivery capacity and proper and timely feedback.

Erwin Beermann

CFO at FibrXL

Cooperative global TP services

Quantera Global provides us with excellent transfer pricing services, which we use as part of our propositions towards our global clients. We appreciate their open and cooperative style of working together. They are always available to brainstorm on tp matters, discuss practical approaches and provide global insights.

Bart Le Blanc

Partner at Norton Rose Fulbright LLP

Pragmatic TP policy guidance

Quantera Global helped us setting up our transfer pricing and financial transactions policy from scratch in an understandable and pragmatic matter. Their expert knowledge and guidance helped us navigate through the different options available. Through their flexibility and outside-the-box thinking we met our transfer pricing obligations.

Andreas Oberegger

Director of Finance and Accounting at BRYTER

Pragmatic intra-group analysis

Quantera was able to help us with analysing our business, and determining the best way forward with respect to our intra-group transactions, in a very pragmatic and cost-efficient way.

Gerben Muntinga

Group Tax Director at Mediq

Why is TNMM widely used in transfer pricing?

TNMM is:

- Easy to apply

- Leaves relatively small results for routine entities

- Prevents losses in multiple jurisdictions

- Typically tax efficient while reducing chances on audits

Tax authorities have an information disadvantage and can more easily dispute other TP methods than the TNMM. It’s often more difficult for tax authorities to judge whether the entity in their jurisdiction is responsible for, for example, losses, or whether that’s caused by factors like budgeting.

This makes that tax authorities are typically in favor of this method. In addition, the easiest way to increase your tax cash out is to have losses in multiple jurisdictions and (assuming a profitable group) consequently high profits in other jurisdictions. The TNMM ensures a small profit in various routine entities and that the residual result is centralized.

In addition, it is relatively easy to implement and maintain, and can be applied to most function/service types.

Pros and Cons of Transactional Net Margin Method

| Pros of TNMM | Cons of TNMM |

|---|---|

| Widely accepted by both tax authorities and taxpayers | Less insight into actual entity performance |

| Predictable results for routine service or distribution entities | Limited incentive for operational improvement (net margin is pre-set) |

| Applicable across industries and functions | Not always suitable for unique/high-value transactions or intangibles |

These limitations can sometimes be addressed through internal management reporting, but they remain a consideration in method selection.

We are here of you need a:

Sparring partner

Sparring partner Many of our clients are experiencing various developments in their business. They like to have a sparring partner who understands their business and its position and who can provide pragmatic advice in a quick and efficient way by addressing only the needs of the company. We enjoy being a sparring partner and are […]

Transfer pricing analysis

All transactions between related entities should be at arm’s length. This is a very important principle in international tax law. A transfer pricing analysis is required to determine the arm’s length price. The tp analysis will show whether there are opportunities and possible threats within the current transfer pricing policy.

Strategic sessions

In the strategic session, our experts gain a deep understanding of the composition and structure of your company, even in the most complex situations. Our team is specialised in understanding your business. The strategic session can focus on a specific topic you would like to focus on or your overall transfer pricing policy.

How can we help you?

Fill out the contact form or visit our FAQ.